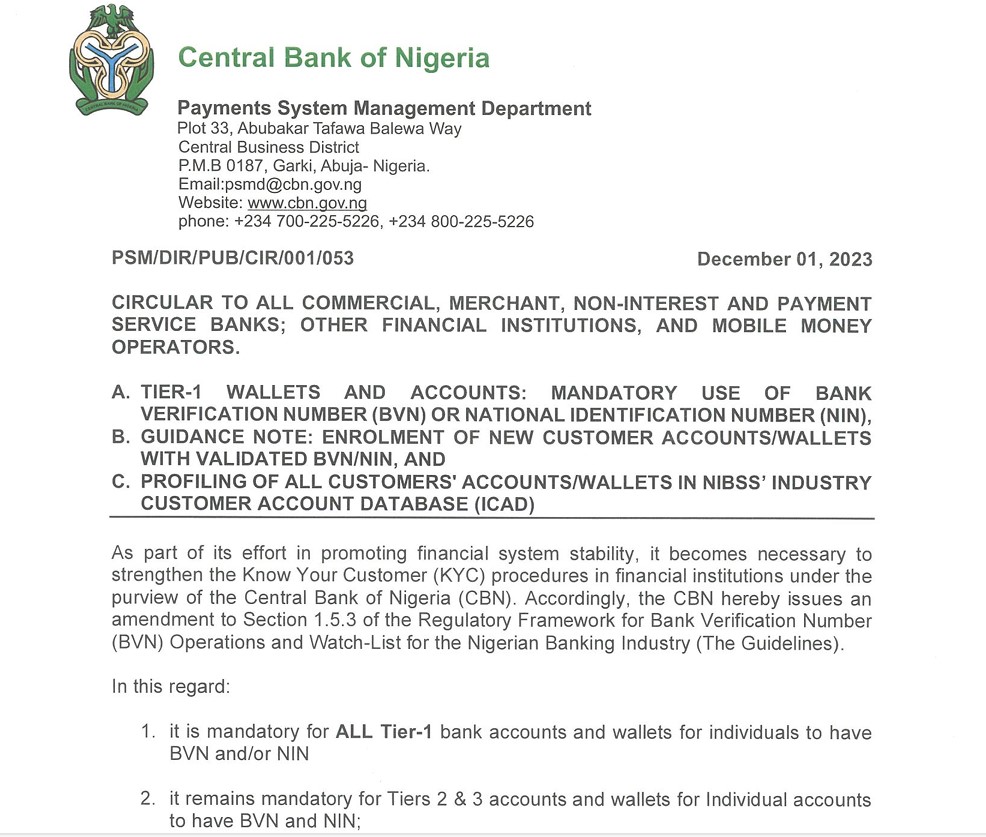

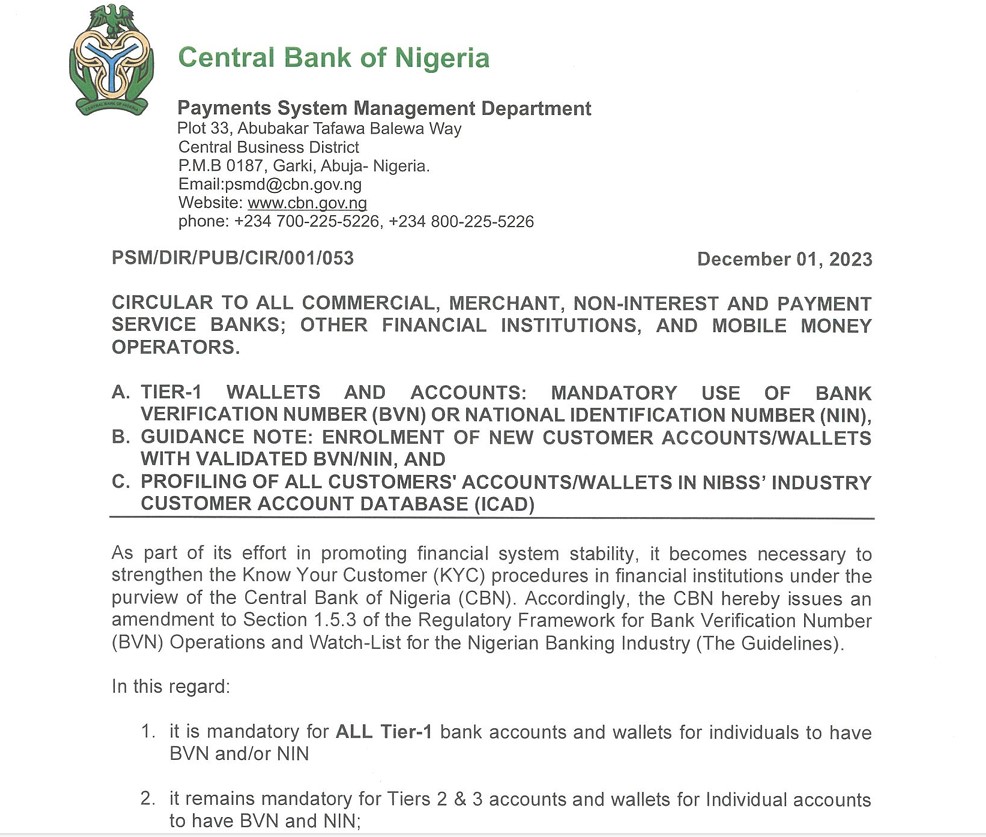

The Central Bank of Nigeria has released a new circular that reshapes how Tier‑1 accounts and wallets must be created, profiled, and managed across the financial ecosystem. These rules affect fintechs, mobile money operators, agents, and any business offering digital financial services. The goal is simple: strengthen KYC, reduce fraud, and ensure every customer is properly identified.

This breakdown highlights the key points of the memo and what they mean for your operations.

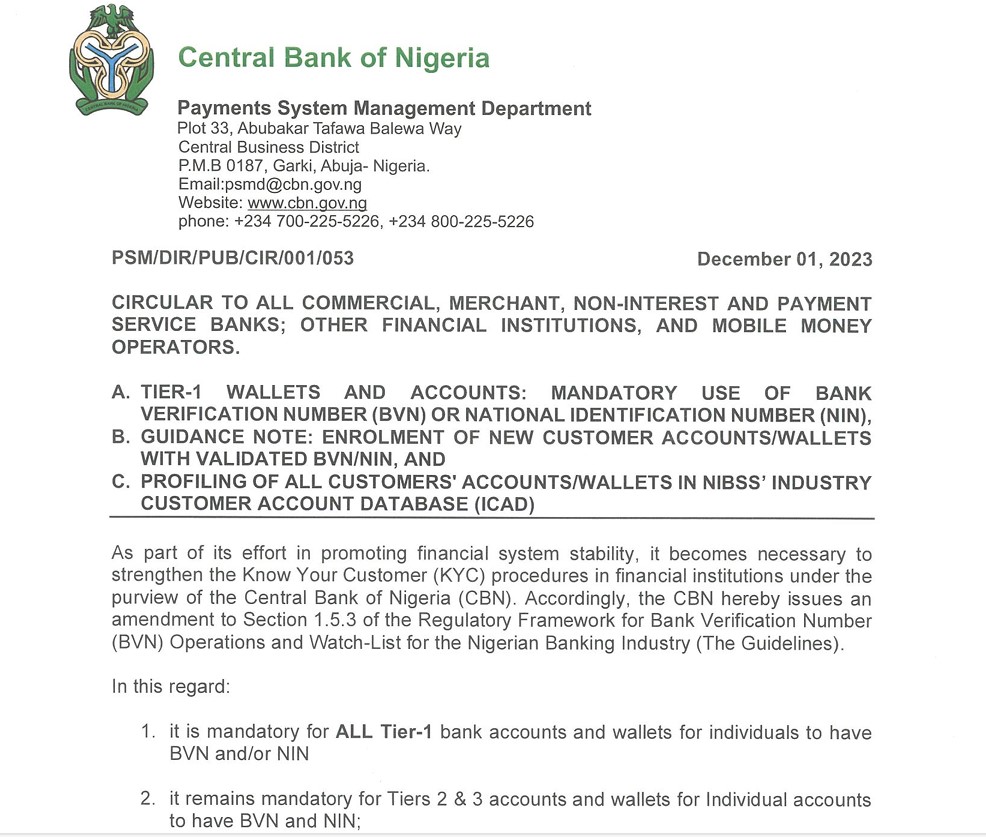

Key Points from the CBN Circular

1. Stricter KYC Requirements for Tier‑1 Accounts

Tier‑1 accounts and wallets must now follow clearer, more consistent KYC rules.

- Customers must provide minimum identification details before activation.

- Financial institutions must verify these details before allowing transactions.

- Anonymous or poorly profiled accounts will no longer be permitted.

2. Mandatory Customer Profiling

The circular emphasizes proper customer categorization.

- Customers must be profiled based on risk level, transaction behaviour, and source of funds.

- Wallet providers must maintain updated customer information at all times.

- Any suspicious or inconsistent profile must trigger enhanced due diligence.

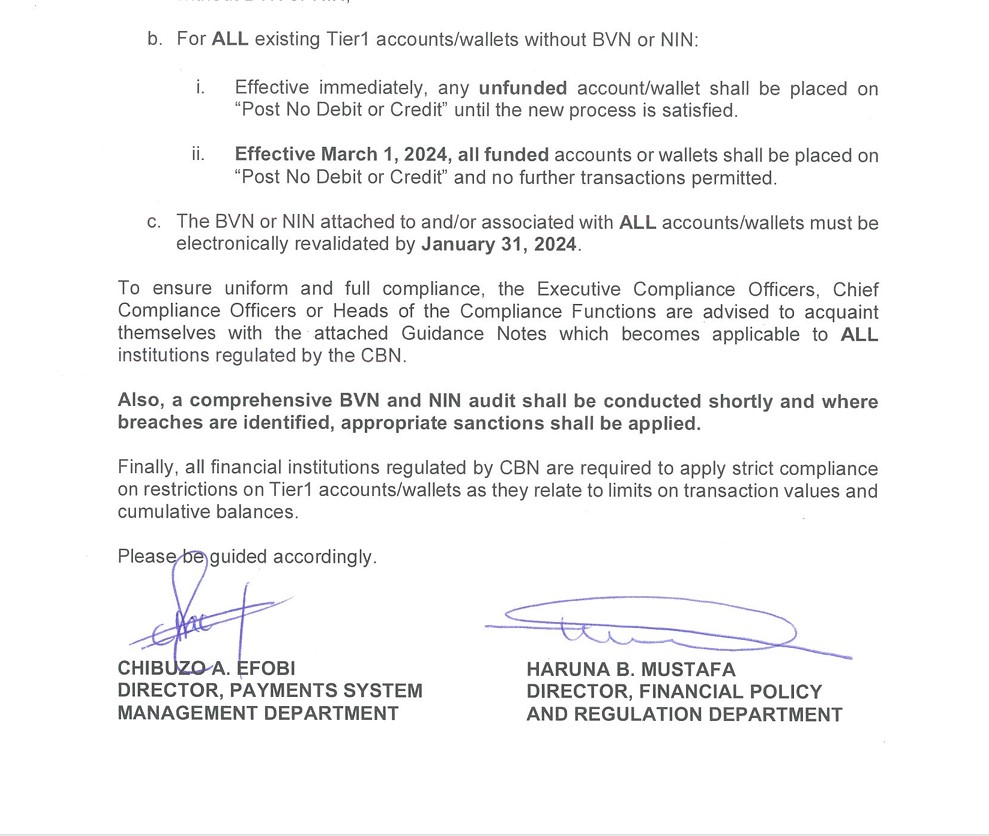

3. Limits on Tier‑1 Wallet Transactions

Tier‑1 accounts remain low‑KYC accounts, so the CBN is enforcing stricter limits.

- Transaction limits must be applied consistently across all platforms.

- Providers must ensure customers do not bypass limits by opening multiple wallets.

4. No More Multiple Tier‑1 Wallets for One Customer

The memo discourages customers from holding several Tier‑1 wallets across different platforms.

- Providers must implement systems to detect duplicate identities.

- BVN/NIN validation becomes more important for preventing duplication.

5. Mandatory Use of BVN or NIN

Every Tier‑1 account must be tied to a valid BVN or NIN.

- Wallets without verified identity numbers must be restricted or closed.

- Providers must integrate real‑time verification APIs.

6. Enhanced Monitoring of Transactions

The CBN expects stronger fraud‑monitoring systems.

- Providers must track unusual patterns, rapid transfers, or suspicious inflows.

- Any red flags must be reported through the appropriate regulatory channels.

7. Responsibility on Fintechs and Agents

The circular places accountability on service providers.

- Agents must follow proper onboarding procedures.

- Fintechs must ensure their platforms comply with all KYC and AML rules.

- Failure to comply may lead to sanctions or service restrictions.

Airtime2Cash remains committed to providing a safe, fast, and transparent platform for all users. These new CBN requirements help protect you from fraud, impersonation, and unauthorized transactions. By completing your KYC with your ID, BVN, and NIN, you’re not just meeting regulations — you’re securing your money and ensuring uninterrupted access to our services.